“Budget Freeze Is Proposed” from Tuesday’s issue of The Wall Street Journal has a chart showing the point that Joe raised on class on Wednesday: that Obama is proposing to freeze something that he’s already jacked up.

Thursday, January 28, 2010

Wednesday, January 27, 2010

Who Was Hayek?

Adam asked this before class. I’ll trust that you can go out and look him up on Wikipedia yourselves, but a good site written by economists sympathetic to his positions is in The Concise Encyclopedia of Economics.

Obama’s “Budget” Freeze

This sounds good. It is good. But it isn’t as good as it sounds.

It’s also a gimmick. In Obama’s defense, it’s a gimmick that others have used.

The problem is that the “budget”, as defined here, is not the whole budget but just the discretionary part. This is the portion that Congress can change just by passing a bill that changes a dollar value.

Unfortunately, there are also parts of the budget that are non-discretionary. These are areas where there is some formula determining payments, and that formula is not so easy to change (not impossible, just difficult and unlikely).

For example, discretionary spending is something like disaster aid for Haiti. Non-discretionary spending is something like cost of living adjustments (COLA) to social security checks (these are tied to the CPI).

The reason this freeze is not as good as it sounds, is that only about 1/6 of the budget is discretionary. The other 5/6 will increase because the laws governing it include automatic increases that don’t require anyone’s approval.

MORE INFORMATION: Argentina

I forgot to mention in yesterday’s post that Argentina actually moved from a politically controlled central bank to a very independent one in the 1990’s, and did very well.

But … it’s a popular opinion when the economy goes bad to blame bankers because … well … um … because a lot of people hold to the childish belief that bankers are always bad guys.

So, one of the first things that Argentina did early this century was to repoliticize it’s central bank. Their economy was already down, so this probably didn’t make things worse. But, it does make the ultimate recovery harder. We’re seeing that now.

Tuesday, January 26, 2010

Political Control of Central Banks

I had mentioned in passing a few weeks ago that a lot of evidence has accumulated over the last 30 years showing that independence of central banks from the political process is associated with higher growth.

This is playing out in a big way in Argentina over the last week. President Kirchner (who – get this -succeeded her husband, President Kirchner) fired her central bank president because he wouldn’t let the government access, and presumably spend, the foreign reserves (currency of other countries – primary the U.S.) held by the central bank. He refused to be fired, and got a judge to reinstate him. The Argentine Congress is on his side. She put up guards to keep him from work. Oh … FWIW … her husband wants to run for President again in the next election.

There have also been moved in South Korea, and Japan to reduce the independence of central banks. Opposition to Bernanke is also, in part, a gambit to reduce independence (it probably is not an accident that his reappointment was in play again only after a major electoral defeat).

There are many sources you can read on these events in both The New York Times and The Wall Street Journal, and you should search a few out. You can start with the front page of the latter from Monday, which featured two of them.

Yes. This Is Testable.

The video is serious; it premiered at the meetings of the American Economic Association a few weeks ago.

It was the idea of Russ Roberts, a professor at George Mason University. Russ uses his academic position eclectically: he’s published 3 novels featuring economic thinking.* He was also one of the earliest economics bloggers, and now writes at Cafe Hayek. He was also podcasting when no one knew what it was; check out his EconTalk site.

Here is a podcast from National Public Radio discussing the development of the video: it started with a video producer from Spike TV (‽ ‽ ‽) who liked to listen to Russ’s podcasts. The first 3 minutes is (tolerable) small talk. About 11 minutes they discuss showing it to Ke$ha … who liked it (and even passed a pop quiz). Roberts even critiques Tik Tok. There’s also an article that covers most of the details.

* I liked and recommend The Price of Everything: A Parable of Possibility and Prosperity and The Choice: A Fable of Free Trade and Protection (3rd Edition)

. I haven't yet read The Invisible Heart: An Economic Romance

.

Sunday, January 24, 2010

Real GDP Graphic

The January 22 issues of The Wall Street Journal has a cool graphic comparing the sizes of countries’ economies:

This is from a piece about Chinese growth entitled “China Targets Inflation as Economy Runs Hot”.

Wednesday, January 20, 2010

How Leftist Is Obamacare?

We discussed briefly in class how both parties in America have moved to the right over the last 30 years; so that Clinton was more conservative than Nixon or Ford.

David Leonhardt’s January 20th piece in The New York Times entitled “Centrist, and Yet Not Unified” echoes this point about the current healthcare bill.

The current versions of health reform are the product of decades of debate between Republicans and Democrats. The bills are more conservative than Bill Clinton’s 1993 proposal. For that matter, they’re more conservative than Richard Nixon’s 1971 plan, which would have had the federal government provide insurance to people who didn’t get it through their job.

Similar points can be made about other Obama policies:

Mr. Obama wants to undo George W. Bush’s high-income tax cuts, but would keep the basic Reagan tax structure intact.

Major pushes for a national healthcare policy were made under Truman, Kennedy/Johnson, Nixon and Clinton before Obama came along.

The current bills, for better and worse, are akin to a negotiated settlement to this six-decade debate. It would try to end our status as the only rich country with tens of millions of uninsured people, as liberals have long urged. And it would do so using private insurers and government subsidies, as conservatives prefer.

… Clinton pushed for putting a cap on the growth of insurance premiums … Today’s Democrats saw that move as too radical. …

The one big conservative idea that’s largely missing is malpractice reform. But the White House said several times that it was willing to negotiate on this issue.

I have serious doubts about whether the Democrats would negotiate in good faith on that last one, but there isn’t any serious argument that the Republicans were even willing to talk.

FWIW: Personally, I’m ambivalent about the politics here. Currently, both parties lean strongly towards centralization on most issues, so there isn’t as much substantive difference as many think. Bush’s spending record is a good example.

Tuesday, January 19, 2010

David Brooks on Haiti

Brooks is a columnist for The New York Times. His January 15 piece entitled “The Underlying Tragedy” echoed the piece I posted the other day.

This is not a natural disaster story. This is a poverty story. …

… [Obama’s] going to have to acknowledge a few difficult truths.

The first of those truths is that we don’t know how to use aid to reduce poverty. … The countries that have not received much aid, like China, have seen tremendous growth and tremendous poverty reductions. The countries that have received aid, like Haiti, have not.

…

The second hard truth is that micro-aid is vital but insufficient. … By some estimates, Haiti has more nongovernmental organizations per capita than any other place on earth.

Third, it is time to put the thorny issue of culture at the center of efforts to tackle global poverty. …

We’re all supposed to politely respect each other’s cultures. But some cultures are more progress-resistant than others, and a horrible tragedy was just exacerbated by one of them.

Friday, January 15, 2010

Boskin on GDP Fudging

Michael Boskin notes that:

Politicians … who don't like what their data show lately have simply taken to changing the numbers. They believe that their end … justifies throwing out even minimum standards of accuracy. … A CEO or CFO issuing such massaged numbers would land in jail.

He offers a couple of examples:

A commission appointed by French President Nicolas Sarkozy suggests heavily weighting "stability" indicators such as "security" and "equality" when calculating GDP. And voilà!—France outperforms the U.S. …

With Venezuela in recession by conventional GDP measures, President Hugo Chávez declared the GDP to be a capitalist plot …

Boskin is a former Republican cabinet member, so it isn’t surprising that he criticizes the Obama administration (so keep your intellectual guard up).

… President Barack Obama has taken it to a new level. His laudable attempt at transparency in counting the number of jobs "created or saved" by the stimulus bill has degenerated into farce and was just junked this week.

… It seems continually to confuse gross and net numbers. …

… The numbers game being used to justify health-insurance reform legislation … Medicare "savings" and payroll tax hikes are counted twice—first to help pay for expanded coverage, and then to claim to extend the life of Medicare.

It isn’t just Obama either:

… The head of the California Air Resources Board, Mary Nichols, announced this past fall that costly new carbon regulations would boost the economy shortly after she was told by eight of the state's most respected economists that they were certain these new rules would damage the economy. The next day, her own economic consultant, Harvard's Robert Stavis, denounced her statement as a blatant distortion.

I would add that this sort of stuff isn’t unusual, but it may be increasing.

Also, I think that the amount of fudging on GDP is proportional to the focus that we place on it. They fudge because we’re looking. This means that you should be looking at deeper numbers (although in Macro we really do need to focus on the broadest data we can get, whether or not it is solid).

Also, keep this in mind when thinking about China’s economic growth. The Chinese government — with Communist, statist, totalitarian, and nationalist roots — releases data that should not be believed.

Read the whole thing, entitled “Don’t Like the Numbers? Change ‘Em” in the January 14 issue of The Wall Street Journal.

Haiti

It’s difficult to get many people to admit to the importance of economic growth for human well-being. Many deny the importance of improved living standards, and denigrate individual aspects of improved lifestyles in order to criticize the “agenda of capitalists”.

The next time this comes up in casual conversation, you need to think about the Haitian earthquake.

Haiti is the poorest country in the western hemisphere. The U.S. is, of course, the richest. I measure both of those by real GDP. Per capita real GDP is at least 40 times higher in the U.S. than in Haiti.

Haiti has been wrecked by the earthquake, and estimates are that there are tens of thousands of dead, and that the number may go into 6 figures.

In 1989, an earthquake of the same size hit the San Francisco Bay area (it occurred during warm-ups of a World Series game, and was broadcast live – although you didn’t see much other than the picture cut out). Sixty-three people died.

The message here is that a 40:1 improvement in real GDP per capita is associated with something like a 1000:1 improvement in the number of deaths.

To me, this suggests that real GDP is tracking something very important, and in fact is underestimating it.

Monday, January 11, 2010

Unevenness of the Recession

All recessions are uneven. Here is the current one, color-coded by state unemployment rates (from pg. 15 of the January 11 issue of Business Week):

The takeaway from this graphic should not be that the recession is uneven. Instead, the width of the 2 pink categories – 2% – is a lot larger than in past recessions. If we did this for the 2000-1 recession, the whole map would’ve been gray, with only some light pink in the northwest.

If you go to the Bureau of Labor Statistics, they have a servlet that will generate color-coded maps and you can see the difference.

Sunday, January 10, 2010

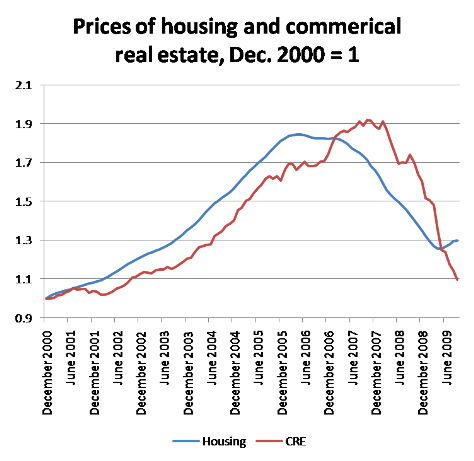

The Twin Real Estate Meltdowns

There is a narrative – especially prevalent in Utah – that the residential real estate bubble and collapse was the result of misguided policies to encourage people who could not afford homes to buy them anyway.

I think this entire narrative is correct, but I think it is overstated.

The reasons are summarized by Megan McArdle in her blog post that links to her article entitled “Capitalist Fools” in The Atlantic:

Yet we can't blame this on predatory lenders tricking the unsophisticated into unwise loans, because these were basically all professionals. Nor can we argue that banks were willing to write toxic loans because they were just going to sell the garbage off to investors; a much smaller percentage of commercial mortgages were securitized (though that percentage did increase as the bubble inflated). And we certainly cannot blame them because they "should have known better" than their borrowers, who usually had more experience than the banks in pricing commercial real estate.

Then there’s this graphic from Paul Krugman:

Click through the above link if you need to (I’m not sure the whole graphic will show).

I have a one caveat and one implication.

The caveat is that the commercial real estate bubble is lagging behind the residential real estate bubble (because outlying subdivisions get built before the neighboring strip malls): if it doesn’t pan out the way that residential real estate has, then the collapse is a different thing than the bubble itself (and will need a different explanation).

My implication is that I’ve played down in class the view that low interest rates were a cause of problems. But … this is exactly the sort of common finding across different markets we’d expect to see if interest rates were a major problem.

Friday, January 8, 2010

Why Is Macro So Hard?

I’ve just reproduced the bullet points from my handout here. I added 3 links to other blog posts which were the sources of the 3 corresponding bulleted points below.

- Everybody has an opinion about macroeconomic issues.

o Most classes you take in college do not cover subjects on which everyone feels entitled to have their opinion respected.

o For example, if you take Organic Chemistry, your weird Uncle Fester is not going to want to argue about it over a holiday dinner – but he might about macroeconomics.

o In many ways, discussing macroeconomics with friends and relatives is like discussing primary education, evolution, religion, or human sexuality – everyone has an opinion, everyone thinks their opinion is right, many people are stubborn about their opinions, and – while most of the opinions are worthwhile – many of them have no foundation whatsoever. They may even know that their viewpoints are incorrect, but they are too wedded to them to change – a psychological condition known as cognitive dissonance.

- Macroeconomic policies have been practiced for thousands of years – so there is a very strong element of “we’ve always done it this way” in the way government officials think about things.

- Our Constitution was written over 215 years ago, yet macroeconomics wasn’t recognized as a separate discipline until 70 years ago – so our government isn’t designed for the timely execution of proper macroeconomic policy. We’ve stapled this to their job description.

- We elect people to do something. In fact, those who have a need to do something are attracted to government. Should we trust them to do the right thing when it is to do nothing at all? We might get better policy decisions if we bought every policymaker a Nintendo Wii to keep them from creating new policies just to stay busy.

- Legislative politics is about finding acceptable compromises, not making the right choices. If it’s hard to order an 8 slice pizza for 3 people that make them all happy, can you imagine trying to formulate macroeconomic policy in Congress or The White House?

- For better or worse, a lot of politics is just adversarial grandstanding. Democrats and Republicans, liberals and conservatives, often say one thing when in power, and the opposite when out of power – kind of like a “friend” who is never hungry until you pay for the pizza.

- The positions of political parties are a mishmash of ideas that have been cobbled together because that combination might attract a majority of the votes. This is like having to choose the better dresser between two old men on the golf course.

- The individual policy positions of a political party are often swapped or reversed through time without consideration of whether the overall platform is consistent. This makes them act like the “mean girls” in high school – they often drop their traditional friends very quickly, and retain allies for loyalty rather than sensibility.

- Most members of Congress and other government officials have little or no background in economics – we primarily elect lawyers to write our laws and then dump responsibility for national economic well-being on them as their primary job. Maybe we should feel sorry for them – they know not what they do. There’s a good anecdote here.

- Just about everyone gets their information about macroeconomic policy from people in the media who have little or no background in economics – some of them probably even went into the media to avoid economics in college, and now they have to talk or write about it for a living. That must ____!

- The media is obsessed with presenting viewpoints that are balanced, in the sense that they try to present experts with different opinions. The problem is that they don’t tell you how much work it took to actually find a different opinion – what if there isn’t any disagreement except from crackpots? Check out this post which shows that you’re more likely to get a split opinion from experts about good news than you are about bad news.

- Policy debates are often lacking answers to really basic questions. How much is this going to cost? Compared to what? How can you be sure? Why do we listen at all if we don’t get answers to these questions first?

- It’s hard to believe, but there’s quite a bit of evidence that policymakers actively suppress the collection of data on controversial policies, but spend freely to collect repetitive information on uncontroversial policies.

- The media are availability entrepreneurs: they are actively seeking out information that is available, and which fits the world view of their consumers. If the information isn’t readily available you won’t hear about, and you won’t hear about it if people won’t listen to that viewpoint. Bad news sells because that’s what we want to hear.

- Many people focus excessively on prices, because they are easy to observe. But, the real action is in quantities: how much did people work, how much did they buy. Increasing and decreasing prices always help one party and hurt another. But, with goods and services, increasing quantities are good, and decreasing ones are bad. More detail here.

- We removed one of the checks and balances from the Constitution that kept special interest politics in check. Prior to the 17th amendment, Representatives represented people, and Senators represented state governments. Now Senators are elected the same way as Representatives, meaning that special interests only have to convince one group (the voters) instead of two (the voters and the states’ government officials). It’s not that different from kids getting more special favors when there’s just one parent around.

The Last 6 Years: A Movie Map

Here’s an evolving map of the U.S. and Canada showing employment changes by month.

Look for:

- The fade out of the 2000-1, with the “jobless recovery” in 2003 and then the strengthening in 2004.

- The effect of Katrina on New Orleans (if you look carefully, you can also see the job increases in places near New Orleans as people moved out and took jobs elsewhere).

- The influx of jobs back into New Orleans as rebuilding commenced in 2006.

- The fact that Detroit’s collapse seems independent of the recession.

- The start of the 2007-9 recession in Bradenton, Florida, and later in Oxnard, California.

- The slow spread of a mild recession in the first 8 months of 2008.

- The rapid increase in unemployment in the last 4 months of 2008.

- The fact that McAllen, in south Texas, has completely skipped this recession!

Leonhardt on Bernanke’s Speech

David Leonhardt is The New York Times economics reporter. He’s pretty good; you should always read him, but he isn’t good enough that you should always accept what he says.

His piece on Bernanke’s speech at the AEA meetings appeared on January 6 and was titled “Fed Missed This Bubble. Will It See a New One?”

He notes that Bernanke is implicitly asking for the Fed to be given more power when they’ve just done a lousy job, and takes the position that reasonable people shouldn’t immediately agree to this.

Leonhardt is most bothered by the fact that the Fed didn’t recognize that there was a bubble in housing prices.

Bernanke’s position is that bubbles are hard to spot until it is too late. I’ll note that this is the consensus among economists.

I think Leonhardt is being self-serving. He is (and kudos to him) one of the people who said there was a bubble. So, his position is influenced by the fact that it was obvious to him. But, it wasn’t obvious to everyone else, and there was considerable disagreement about this in 2004-6.

So, if Leonhardt thinks attacking bubbles is a good thing, it would be useful to ask him 1) what bubbles are out there right now that need attacking, and 2) what are the effects if you attack a bubble and it isn’t one?

I’ll add two points.

First, if we look at the tech stock bubble of 1998-2000, it’s clear that there were many bubbles in individual stocks, but that it is much harder to make that case for the whole market since a lot of the aggregate stock value is still with us today, just spread over a smaller set of firms (e.g., Google, Cisco, Apple, Verizon).

Second, a bubble – by defintion – should be something irrational that can’t be repeated. Except that this is not the first time we’ve had a real estate price bubble in southern California. If this is a repetitive phenomenon, then the whole bubble position has to be thrown out.

Tuesday, January 5, 2010

Some Current Economic Signs

This isn’t a great article, just a decent one to start the semester.

There are lots of signs that the economy is growing again, and fairly strongly at that.

There are lots of worries about some data that still looks bad – wealth, debt, foreclosures, and so on.

The article does discuss the theory of what is going on, but it is one of the purest Keynesian viewpoints I’ve seen in ages.

It does not do a great job of explaining the employment and unemployment situation. it discusses the number by which jobs are expected to increase, and the amount that they decreased, and emphasizes that these don’t match up positively. No mention is made of the fact that this is normal after recessions: firing is a lot easier than hiring.

From “Divergent Views of Signs of Life In the Economy” in the January 5 issue of The New York Times.

Bernanke’s Speech

Ben Bernanke – Chairman of the Federal Reserve – made a speech the other day.

Nothing unusual about that.

What was unusual is that he made it at the annual meetings of the American Economics Association – so the audience was all experts. Ideally, this would make it more thoughtful.

This is a good point to mention a bunch of issues related to what was in the article.

First, there is Bernanke. Many blame him, in part, for the economy’s problems. This has died down a bit, and it now looks like he will get a second term. We have had Fed chairmen before who goofed things up: I’m not sure Martin knew what he was doing, and Miller was a bowed to politics over economics. It’s possible that Bernanke is part of the problem, but this doesn’t seem likely. He isn’t known for jumping to rash decisions. He is known for being demonstrably smarter than just about everyone else. He had Fed experience before taking the job. He had executive experience before taking the job. And … he’s probably the premier living expert on how badly monetary policy was conducted during the Great Depression. Other people might do a better job, but they sure won’t look like better applicants for it.

Some people also blame his predecessor Alan Greenspan. This is funny, since the world spent almost 20 years idolizing his performance. Either his critics were lying to themselves and others then, or they are just being jerks now. This is kind of like criticizing FDR as a president; you can do it, but it’s a stretch, and you’ll probably end up sounding like a hack.

There’s also been a lot of criticism of the Federal Reserve – from both the left and the right. The upshot of most of this criticism is a call for more political oversight of the Fed. This is in spite of the fact that economists spent most of the last 30 years researching how the political independence of central banks was strongly related to positive economic performance. This led dozens of countries to distance their banks from their governments, in imitation of the central banks in the U.S., Germany, Switzerland, the U.K., and New Zealand.

All of these criticisms are worth listening to, and considering seriously. But, I think any serious consideration of them should start with the reasons why we should reject all of the past research on these issues. Think about it: when was the last time you heard a pundit mention that Bernanke was not the best man for the job when it was open, that everyone must have been wrong to think that Greenspan should be reappointed 3 times (by Democrats and Republicans), or that the Federal Reserve needed tighter control because the economy wasn’t vibrant enough the last 25 years?

Now, this article discusses how Bernanke specifically combats the assertion that the financial crisis was caused by interest rates that were too low under Greenspan. Instead, Bernanke cites lax financial regulation, mostly by other agencies.

Not surprisingly, Bernanke’s assertion paints him and the Fed in a nice light. On the other hand, he wasn’t booed by an audience full of people well-versed in both arguments.

I’m not going to take too strong a position on this – it’s early in the semester, but it’s also early in the post mortem of the Great Recession. I will point out that most of the macroeconomics books used at the principles level have large, and increasing, treatments of the lax oversight of government sponsored entities involved in financial regulation. This stuff started showing up in books 15 years ago, so it isn’t like the experts didn’t see problems coming. Also, the financial bubble has never seemed to be nationally even, and its easier to see how regulation could vary by location than it is to argue that Fed policy varied by location.

And … I want to stay somewhat non-committal on low interest rates. Maybe we’ll decide that was a problem when all the numbers are in. For now, though, I am highly suspicious of this position. For my part, it falls too neatly into the common argument that things would have been better if only we’d been harder on ourselves earlier. This is a moral position that people have been pushing for thousands of years, and there isn’t a lot of empirical support for it: that’s why it is couched as a moral rather than an empirical argument. But … economics is about data, and without a lot of other financial systems that blew up because of low interest rates, I tend to think this viewpoint is not very strong.

Lastly, I’ll add a seldom mentioned point. If the low interest rate as a cause story is true, then we are in for some very rough times ahead. The reason is that low interest rates are indicative of loanable funds swamping viable projects that people might borrow to finance. Why on earth would this be happening? Well, first off, the world is filthy rich in ways we couldn’t imagine in the past. So, there’s a lot of money out there. Second, a lot of that money is coming from places like China and Arab countries, who don’t have societies that generate a lot of viable projects. So, there money comes here. Neither one of these is going to go away. So, low interest rates won’t either. Thus, if you take the low interest rates as a cause argument seriously, the future looks like one of common and severe financial crises. To me, this doesn’t seem plausible.

Read up on this in “Lax Oversight Caused Crisis, Bernanke Says” in the January 4th issue of The New York Times.

Subscribe to:

Posts (Atom)