I was writing this from home on Tuesday when we lost internet connectivity for about a day.

***

The rating agency Fitch downgraded Russian bonds. This seems to be in anticipation of default being declared if the Russians try to make interest payments with rubles.

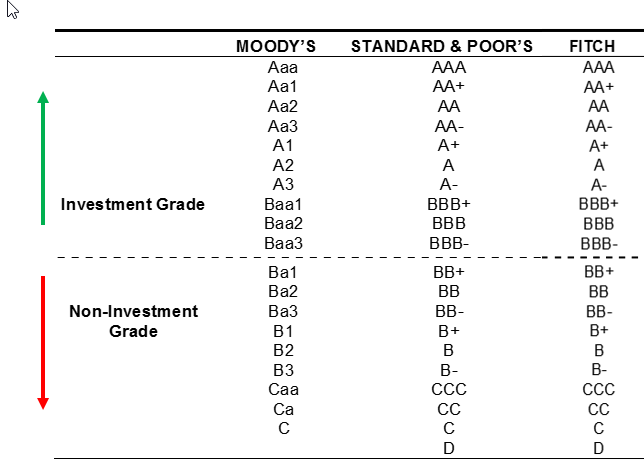

Each rating agency has a slightly different scale for rating bonds. But charts like this one are easy to find:

Fitch downgraded Russian bonds from somewhere in the B's to C. Of course, the bottom of the list indicates near-certainty that the issuer of the bonds will default on them.

Investment grade means that firms that have some fiduciary responsibility towards clients are allowed to buy. Non-investment grade bonds are commonly and pejoratively called "junk bonds". Lots of people and firms buy those for their higher yields, they're just generally not doing that with other peoples' money.

Bonds towards the bottom of the list have to promise to pay a higher rate of interest at the time of issue in order to entice potential buyers to commit to their risk.

Once bonds are in circulation, and can be resold from the initial buyer to anyone else, the ratings agencies re-evaluate them periodically so that inattentive holders have a clue.

Generally speaking, when it becomes less likely for a bond to pay its income stream, investors have been watching the news and already see this coming. So holders of those bonds become interested in getting rid of them, and are willing to accept a lower price to get rid of them. When the price gets low enough, some bargain hunter may decide the risk is worth the lower price. As discussed in principles classes, bond prices and interest rates go in opposite directions. So price and ratings move together, and interest rates (yields) and ratings move in opposite directions.

While the rating agency decisions make the news, they often reflect (rather than lead) a reality in that market that holders are trying to get rid of the things.

***

Of course, someone might know a bond they hold is getting riskier. But they might think it's worth something more than what they can get for it. This is where the CDS market I've mentioned a couple times in class comes into play.

If the bond issuer does not make an appropriate payment, bondholders can ask for a determination of whether or not that is considered a default. If it is, the entity that gambled and sold the CDS to the bondholder pays up. If it isn't, the CDS continues to be valid until it expires.

Russia has interest payments starting to come due. Some of their bonds stipulate that the interest may be paid in rubles. But bondholders may make the case that exercising that stipulation is a form of default because at the time they agreed to it, no one envisioned Russia behaving bizarrely. A committee was set to meet on this issue as early as Wednesday the 9th.

No comments:

Post a Comment